Lovable Hits $400M ARR With 146 Employees

Swedish AI app builder Lovable crossed $400 million in annual recurring revenue in February, adding $100 million in a single month with a headcount that wouldn't fill a mid-sized office.

TL;DR

- Lovable crossed $400M ARR in February 2026, adding $100M in a single month

- The company has 146 employees - roughly $2.7M in annual revenue per head

- Backed at a $6.6 billion valuation after a $330M Series B in December 2025

- Investors include CapitalG, NVIDIA, Salesforce, Databricks, and Khosla Ventures

- The numbers challenge every assumption about what a software company needs to scale

The Swedish startup Lovable crossed $400 million in annual recurring revenue in February 2026, according to figures disclosed by CEO Anton Osika. The company says it added $100 million in a single month. It has 146 employees.

Those three numbers don't sit comfortably together in any conventional model of how software businesses scale. They're worth examining closely.

The Revenue-per-Employee Calculation

At $400 million ARR with 146 staff, Lovable's implied revenue per employee runs to roughly $2.7 million annually. For comparison, Salesforce - widely regarded as an efficient enterprise software operation - generates around $500,000 per employee. Even Cursor, which made headlines in March after hitting $2 billion ARR faster than any SaaS company in history, has a more conventional staffing ratio.

The numbers reflect what Lovable actually sells: an AI-powered app builder that lets non-developers and small teams produce full-stack web applications through natural language. The company sits at the centre of the vibe-coding movement, which has pulled in users who previously had no path to building software on their own.

Product-led growth means Lovable doesn't need a large enterprise sales force. Users sign up, pay, and build. The marginal cost of picking up a new customer is low. The marginal cost of serving them is mostly compute.

Lovable CEO Anton Osika at Web Summit 2025 in Lisbon, before the company's most explosive growth phase.

Source: techcrunch.com

Lovable CEO Anton Osika at Web Summit 2025 in Lisbon, before the company's most explosive growth phase.

Source: techcrunch.com

What the Series B Bought

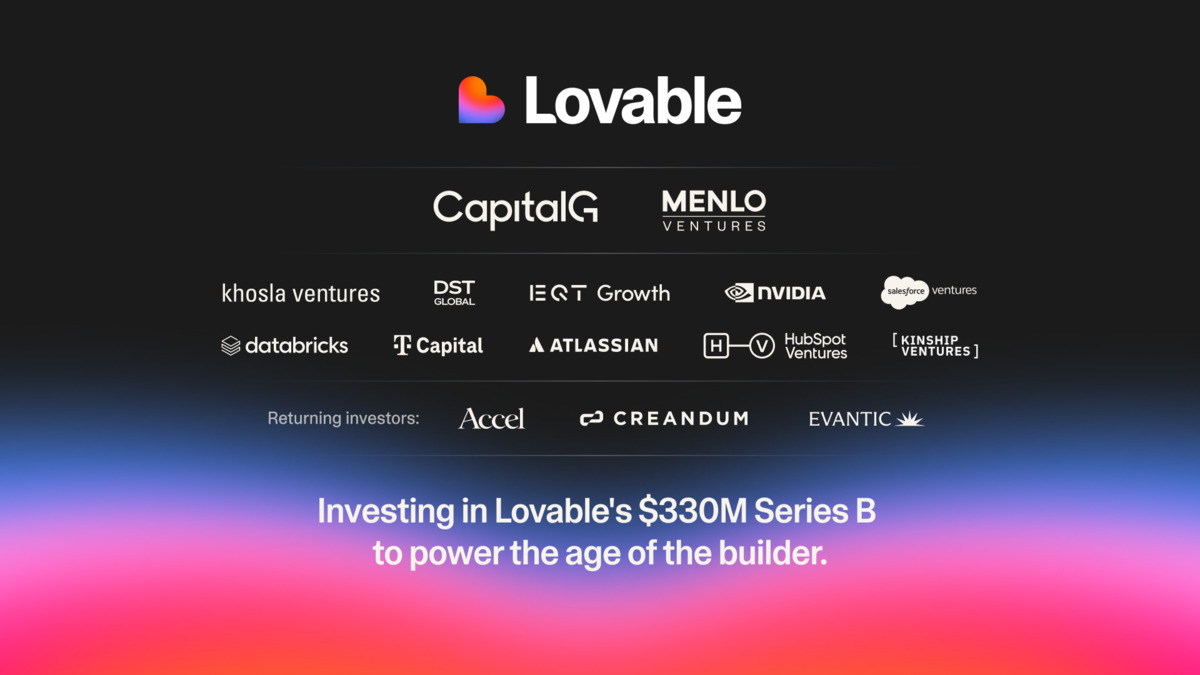

Lovable closed a $330 million Series B in December 2025, led by CapitalG and Menlo Ventures' Anthology fund, at a $6.6 billion valuation. The deal brought in strategic investors who are also distribution channels: NVIDIA, Salesforce, Databricks, Atlassian, and HubSpot all participated. Deutsche Telekom joined too, with Khosla Ventures and DST Global.

That investor list tells you something. Salesforce is backing a company that sells a tool capable of replacing a Salesforce implementation. One case study on Lovable's own blog describes a startup that swapped a $40,000 Salesforce contract for a Lovable-built CRM. Salesforce presumably calculates that the alternative - staying out of the AI-native software boom - is worse.

The use of funds is pointed at three areas: deeper integrations with tools like Notion, Linear, and Jira; enterprise governance and collaboration features; and production infrastructure including hosting, databases, authentication, and payments.

That last item matters. Lovable is moving from a tool that builds prototypes into a platform that hosts and runs production software. That changes the unit economics, the liability profile, and the competitive surface area. It also dramatically increases lock-in.

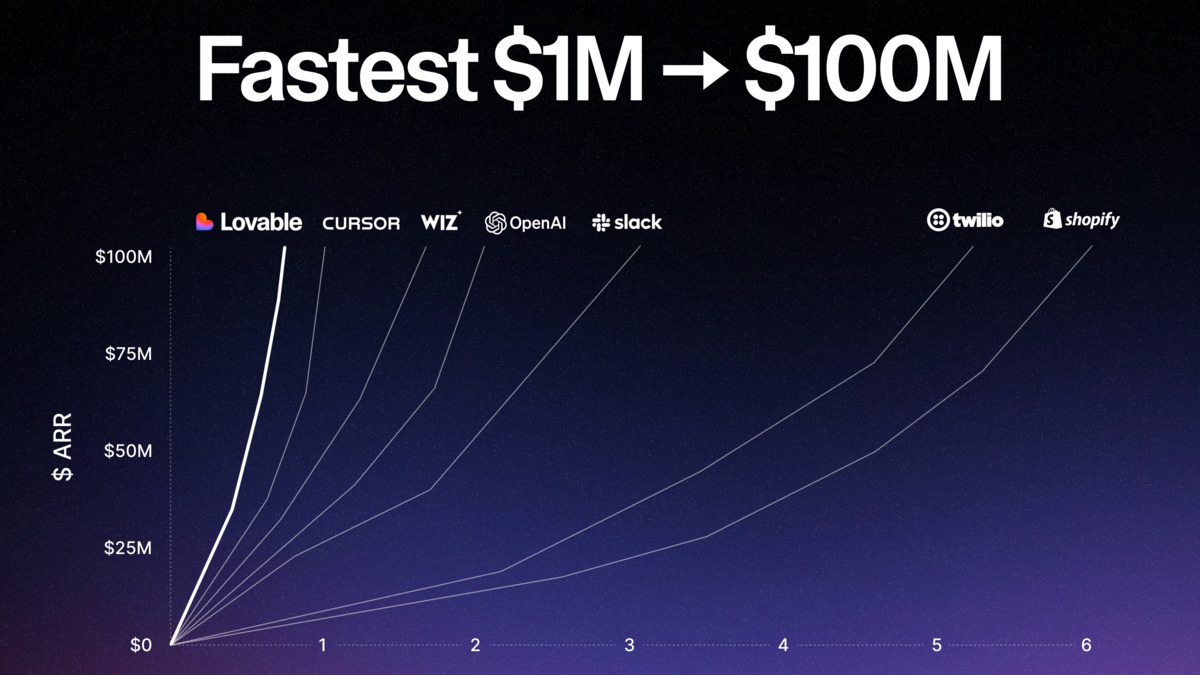

Lovable's early growth trajectory from $1M to $100M ARR, among the fastest recorded for any software company.

Source: lovable.dev

Lovable's early growth trajectory from $1M to $100M ARR, among the fastest recorded for any software company.

Source: lovable.dev

The Valuation Question

A $6.6 billion valuation on $400 million ARR implies a revenue multiple of roughly 16.5x. That is high. For reference, Cursor's $2 billion ARR valuation was reported at around 9-10x revenue. GitHub Copilot, the tool Cursor is displacing, is embedded inside a company valued at around 7-8x its AI-adjacent revenue contribution.

Lovable's multiple is partly a bet on growth rate. If the company sustains even a fraction of its current growth rate through 2026, the entry multiple compresses fast. The investors who led the round - CapitalG is Alphabet's growth fund, so these aren't unsophisticated risk-takers - presumably ran those scenarios.

There's a meaningful counterargument. Lovable's revenue is mainly from individual developers and small teams on subscription plans. Enterprise ARR, which carries more predictable retention, is a smaller slice. The February numbers may also include a seasonal spike tied to New Year product launches and the general wave of vibe-coding enthusiasm that has swept developer communities since late 2024.

At $2.7 million in annual revenue per employee, Lovable is operating in a regime that most software businesses will never reach. The question is whether it stays there.

What the Numbers Mean for the Industry

Lovable's metrics land in the middle of a wider argument about what AI is doing to software company headcount. Naval Ravikant's declaration that AI is eating software and the broader SaaS market selloff are on one side. On the other, skeptics point out that most AI-native tools still face the same churn, support, and sales challenges as traditional software.

Lovable doesn't settle that argument. But it gives the AI-native camp a data point that's hard to dismiss. The company went from zero to $400 million ARR in roughly 14 months. It did it with a team small enough that the CEO can credibly say he knows every employee's name.

Stripe had roughly 350 employees when it crossed $400 million ARR. Shopify had more than 2,000. HubSpot crossed that mark with a sales org that took years and hundreds of millions of dollars to build.

None of those comparisons are perfect. Lovable's average revenue per user is lower, its churn is less well-documented publicly, and its path to enterprise contracts is still being built. But the direction of travel is clear, and it's uncomfortable for anyone running a software business that still operates on pre-AI assumptions.

Lovable's Series B investor roster, showing participation from companies including NVIDIA, Salesforce, Databricks, and Atlassian.

Source: lovable.dev

Lovable's Series B investor roster, showing participation from companies including NVIDIA, Salesforce, Databricks, and Atlassian.

Source: lovable.dev

The Risk Hiding in the Model

The security concerns around vibe-coded applications remain unresolved. Research from early 2026 found that AI-produced codebases have significantly higher rates of common vulnerabilities than developer-written code. Lovable itself received pointed criticism in a detailed review of the platform for pushing users toward production deployments without enough friction around security basics.

Lovable's move into production infrastructure - hosting, authentication, payments - is also a move into regulated territory. A breach affecting a production app running on Lovable infrastructure would land differently than a breach in a prototype.

That's not a reason to dismiss the revenue numbers. The company's growth is real. But the $6.6 billion valuation assumes that the enterprise governance features being built with Series B money will arrive before the security incidents that would undermine them.

If you're investing in Lovable, you're betting on execution speed. If you are competing with Lovable, you're betting on the problems catching up before the revenue does.

In February, the revenue won the month by a margin of $100 million.

Sources: