Wall Street and Google Pool $5B to Rival CoreWeave

Blackstone commits $5 billion to a new Google joint venture selling TPU compute-as-a-service, directly challenging CoreWeave with Wall Street capital and Google's chip stack.

Blackstone is betting $5 billion that enterprises will pay for Google's custom AI chips if someone else builds the data centers.

The two companies announced a joint venture on May 18 to create a new U.S.-based company selling TPU compute-as-a-service. Blackstone puts up the money and manages the real estate. Google supplies the Tensor Processing Units, software stack, and services. The new company's first CEO is Benjamin Treynor Sloss, who spent more than 20 years building Google's infrastructure and coined the term "site reliability engineering."

Layer in the implied debt financing and the venture's total capital could reach $25 billion - making it the first competitor to CoreWeave with equivalent firepower.

TL;DR

- Blackstone commits $5 billion in initial equity; total capital including debt financing could hit $25 billion

- New company sells Google TPU access as a standalone compute-as-a-service product, separate from Google Cloud

- Benjamin Treynor Sloss, Google's former infrastructure chief, leads as CEO

- First 500 MW of capacity targeted for 2027

The Deal Structure

This isn't a typical cloud partnership where a hyperscaler resells capacity under another brand. The new company is a stand-alone entity. Blackstone holds majority control. Google contributes TPU chips, proprietary software, and services, but not the balance sheet.

That split matters economically. Google is already on the hook for $175 to $185 billion in capex in 2026 across its full operations. The JV lets it capture a share of the $700 billion in AI infrastructure spending projected across Big Tech this year without adding proportionally to that number. For investors and analysts tracking Google's capital allocation, it moves TPU distribution off the core balance sheet.

For Blackstone, the logic is different and simpler. The firm manages $1.3 trillion in assets and is already the world's largest alternative asset manager and global data center investor through its QTS Realty portfolio. It has existing positions in OpenAI, Anthropic, and SpaceX. This deal plugs those infrastructure bets directly into the AI hardware stack rather than just the real estate surrounding it.

"We see a generational opportunity to invest capital at scale building AI infrastructure," said Jon Gray, President and COO of Blackstone.

The Comps

The joint venture enters a market where the incumbent has a major head start. CoreWeave committed up to $35 billion in data center spending for 2026 alone, funded largely by debt. Meta signed a $21 billion deal with CoreWeave in April, giving it a major anchor customer. NVIDIA invested $2 billion in CoreWeave in January, turning the neocloud into an extension of its own distribution strategy.

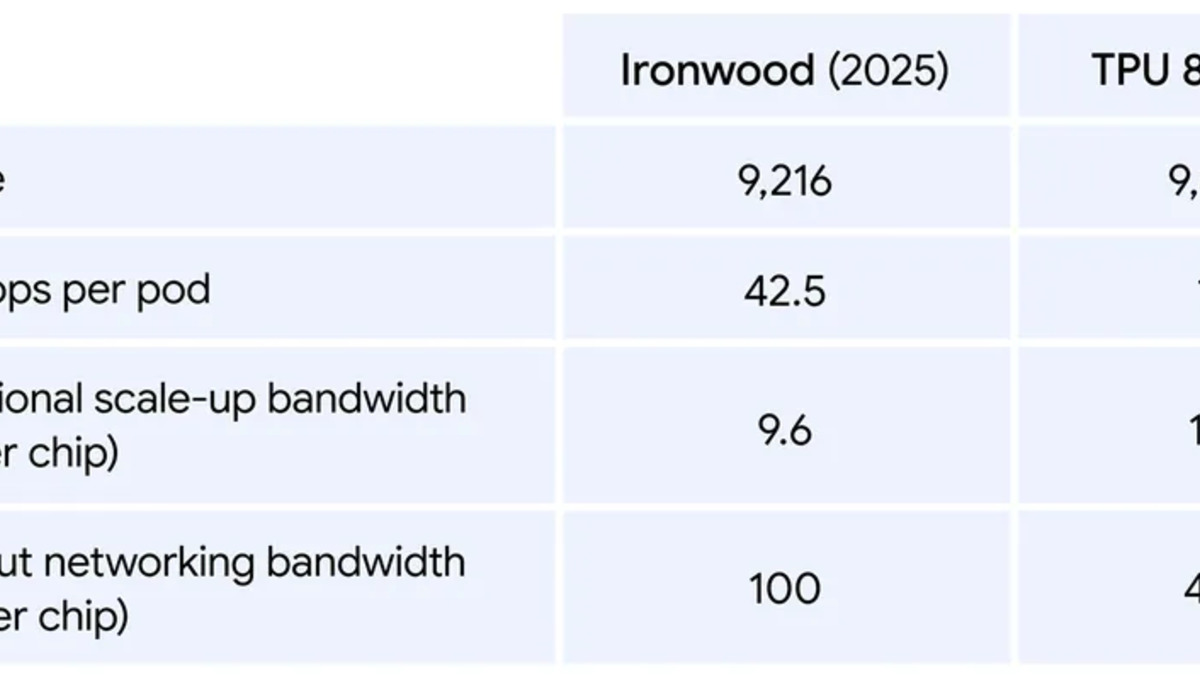

Google's TPU 8 chips are the hardware central to the new venture. The 8t training variant scales to 9,600 chips with 121 ExaFlops of compute per pod.

Source: blog.google

Google's TPU 8 chips are the hardware central to the new venture. The 8t training variant scales to 9,600 chips with 121 ExaFlops of compute per pod.

Source: blog.google

| Google-Blackstone JV | CoreWeave | |

|---|---|---|

| Compute | Google TPUs (8th gen) | NVIDIA H100/H200 GPUs |

| Capital | $5B equity; ~$25B total | Public markets + NVIDIA stake |

| Live capacity | 500 MW targeted by 2027 | Global, operating now |

| Business model | Compute-as-a-service | Dedicated GPU cloud |

| Chip source | Google (proprietary) | NVIDIA (third-party) |

Google's TPUs are not new to external customers. Anthropic already runs significant workloads through a multibillion-dollar TPU supply agreement with Google. Google has been building out external-facing TPU capacity - including a full eight-chip roadmap covering both training and inference that spans the next two years.

What's new is the financial structure. Until now, Google sold TPU access only through Google Cloud, meaning customers used it inside Google's full product stack. The JV creates a standalone TPU vendor - closer in model to CoreWeave's dedicated GPU cloud than to a hyperscaler's bundled offering.

Thomas Kurian, CEO of Google Cloud, framed the deal as expanding access:

"This joint venture with Blackstone helps meet growing demand for TPUs, which are optimized specifically for efficiency and performance in the AI era."

Who Benefits

Google gets a new distribution channel without loading more onto its own capex. It also answers the standing criticism that its chips are only accessible inside its cloud ecosystem. Three customer types are most likely to shift toward the JV: foundation model labs that want to diversify away from NVIDIA silicon, enterprise GPU users already evaluating TPU economics, and sovereign AI buyers that are blocked from NVIDIA hardware by U.S. export controls.

Blackstone gets a technology partner with a decade-long lead in custom AI silicon. Its BXN1 infrastructure group has been building toward exactly this kind of placement - hardware-backed infrastructure with defensible supply characteristics. Jas Khaira, head of Blackstone N1, was direct about the thesis:

"Capital alone doesn't build category-defining platforms - the right partner, the right structure, and the conviction to underwrite singular opportunities do."

Enterprise customers gain a third option. The AI compute market has largely forced a choice between NVIDIA-backed clouds and Google's managed services. A standalone, well-capitalized TPU vendor changes that.

Who Pays

CoreWeave is the obvious target. Its entire valuation rests on being the preferred non-hyperscaler GPU cloud. The Google-Blackstone JV is capitalized at comparable scale, backed by a chip architecture Google has refined for a decade, and led by someone who helped build the infrastructure running Gemini. One analyst called it "the most credible competitor that category has yet seen."

NVIDIA takes a subtler hit. Its $2 billion stake in CoreWeave was designed to cement GPU primacy in the neocloud market. A well-funded competitor running Google silicon at data center scale is the scenario that investment was meant to hedge. Amazon's custom Trainium chips have already reached a $20 billion annual run rate, growing 40% quarter over quarter. The JV opens a second front.

Smaller GPU cloud providers - those running on rented NVIDIA capacity without proprietary chips or comparable capital depth - face a harder pitch to enterprise customers if two $25 billion-plus options exist from better-capitalized players with their own silicon.

The venture's first 500 MW of capacity is targeted for 2027, with plans to scale markedly beyond that.

Source: thenextweb.com

The venture's first 500 MW of capacity is targeted for 2027, with plans to scale markedly beyond that.

Source: thenextweb.com

The real test arrives when the first 500 MW goes live in 2027 and enterprise customers have to choose between familiar NVIDIA hardware and a TPU cloud backed by Google chips and Blackstone's $1.3 trillion balance sheet.

Sources:

Last updated